The South Korean Financial Services Commission (FSC) announced Sunday, November 5, that they will impose a temporary short-sell ban on both KOSPI 200 and KOSDAQ 150 stocks effective November 6th until end of June 2024.

The FSC enacted the short-selling ban in order to review the current short-selling system. According to the FSC, institutions are engaged in naked short-selling, which is disallowed due to current Korean regulation. Regulators believe it leads to an unfair environment for market participants.

The ban’s objective is to give the regulator an opportunity to implement a real-time position check system that can monitor naked short-selling. Short sell bans are not new in South Korea: this is the fourth ban since 2008-2009, with the most recent one occurring in 2020-2021. The first comments regarding a possible ban came on the October 27th by ruling party member Mr. Yoon Chang-Hyun who said, “the time has come to stop short-selling altogether for three to six months and devise fundamental measures.” Following that, FSC head Mr . Kim Joo-Hyun said they will review current short-sell regulations from “square one,” according to Business Korea and other local news sources. The full-scale ban, though, seems to have caught most investors off guard.

Government Communication

The market initially interpreted the above comments to mean a ban was likely imminent, eventually leading the FSC to make a public statement refuting a potential short-sell ban, highlighting on their official FSC website on October 30th, “the push to ban short-selling is not true, so please be cautious in your reporting.” Then on November 3rd the FSC made a second statement specifically denying regulators would enact a short-sell ban.

On Sunday November 5th the South Korea government abruptly changed their view and decided to enforce the ban. This raised questions over the government’s political motives with elections expected in April.

The previous bans have all led to positive market performance: during the 2008 short-selling ban (Oct 2008-May 2009), the Kospi and Kosdaq were up 49% and 91% from their respective bottoms until the ban was lifted. In 2020 (Mar. 2020- Apr. 2021), the Kospi and Kosdaq were up 112% and 122% during the ban. Furthermore, the 2011 short-selling ban was only three months starting from August 10, 2011, but the Kospi and Kosdaq were up 6% and 18% during that period.

In addition, Korean regulators announced November 16 their intention to further restrict short selling rules for institutions, while bringing retail restrictions inline with institutions. The FSC will lower retail collateral requirements from 120% to 105%, while also capping the maximum borrow time on a stock to 90 days for short selling purposes for institutions. These proposals will need to be ratified via the legislative process before being implemented, according to the FSC.

The overall short-selling changes may jeopardize South Korea’s ongoing goal, as ambitious at it may seem, to gain MSCI admission into developed market status.

How can Meraki Help?

Asian Coverage from Hong Kong for Global Managers is One of Our Major Specialities

Korea made this announcement early Sunday in the US and Europe, surprising global investors with the announcement and the timing. Given the Sunday announcement, local time, the timing further complicated the ability to trade objectively and effectively on the Monday morning when Korea opened without a live Asian trading desk.

Risk-driven events like this are inherently difficult to manage and this particular event generated 2-sigma intraday volatility within the markets, while the EV Battery makers collectively moved +23% on the day and single stocks like Ecopro (247540 KS) and Posco FM (003670 KS) reached limit up +30% before the close.

About Meraki Hong Kong

Our local Hong Kong office employs a full trading team available and experienced in all APAC markets. Our traders have worked locally in both Hong Kong and India and collectively have decades of experience in the region and understand the nuances of the Asian markets. Cognizant of information leakage and protecting client orders, our 3:1 client to trader ratio, as well as Meraki’s neutral, unbiased trading structure, allows Meraki to be completely aligned with its clients’ trading objectives. Please call us to provide more market colour and strategic insights.

We remain, sincerely yours, the trading team, Meraki Hong Kong.

Welcome to this episode of “Meet the Meraki Team.”

Meraki Global Advisors LLC, a leading global multi-asset outsourced trading firm, was founded with a rebellious determination to deliver truly conflict-free services to asset managers. At Meraki Global Advisors, our team is our greatest asset, and today, we have a special guest to share his wealth of experience and expertise.

Joining us is Tom O’Leary, Senior Business Strategist of Meraki Global Advisors. Tom brings nearly 35 years of extensive industry experience in strategic planning and business development, leading high performing teams, and integrating information technology for improving processes at companies building and scaling their capital markets business infrastructure. He joins Meraki from HSBC Global Banking and Markets, where he served as Managing Director and Head of Equities for the Americas focusing on managing the equities business across the globe, and a member of the Global Equity Executive Committee. Prior to HSBC, O’Leary was a Senior Managing Director with Bear Stearns in a variety of leadership positions, including Co-Head of the Global Equity Sales Division and Head of International Equities.

In this episode, Tom O’Leary will take us through his journey, sharing valuable lessons learned and how each experience shaped his approach to trading and risk management. This promises to be a captivating conversation with a true industry expert.

“Look, we’re not for everyone. Everybody’s not going to want to do outsourced trading and everybody’s not going to want to do outsourced trading exactly the way that we do it. But Ben Arnold, the founder of the firm decided this is the way we’re going to do it, and I think it’s the purest form of outsourced trading. And this is what we do. It’s the only thing we do. And it’s the only way we do it.”

Let’s dive right in!

Q1: Walk through your history and what roles you have filled over your career?

It’s been a long career. I’ve got nearly35 years of experience in the industry, but really with two long stretches…the first one being at Bear Stearns for 14 years, where I held numerous positions, and the second one being at HSBC for 11 years, where for all 11 years I was Head of Equities in the Americas. But, at Bear Stearns, I started on the Latin American desk as a salesperson. I held numerous positions, one of them was Head of Research for Latin America. I also rose to be the Head of International Equities, and eventually, right before JP Morgan took Bear Stearns over, I was Co-Head of Sales for Equities across the entire equity business.

Q2: What excited you about joining Meraki and outsourced trading?

It really was the quality of the people at Meraki. And even though we’re a relatively small firm, it’s unique in the fact that so many people at the firm have known each other from the industry for many years. Even a couple have worked together earlier in their career. But it’s really the quality of the people, and the quality of the product is the traders. The traders have a wealth of experience from the buy-side that they bring to the table. That was really appealing to me when we are going to be marketing this service and growing this business through a client service business. These guys are actually the product, so they’re what’s important. It’s their experience and the unique services offered that we really sell.

Q3: How has the landscape changed and grown since your time at HSBC?

Probably not so much as change, but certainly things continue to move at an accelerated pace. We mentioned one of the trends in the industry that I think is really driving a lot of key decisions is the cost pressures that both the buy and the sell-side are facing. And those are significant. Those started 10 or 15 years ago, and every time you feel like they’re done, they continue to accelerate.

When those cost pressures come on the sell-side, you immediately look to headcount to reduce because you usually have vast teams where you can make those reductions. For asset management, those decisions are even a little bit more challenging. They’ve got to make key decisions like-

Do I add another trader? Or do I add another analyst? Do I add another portfolio manager? Are we going to be looking at a different region?

…So, those cost pressures are real. Also, the rate of change on the technological rates of change continues to be significant for the business. These are two major mega-trends that I just don’t see slowing down whatsoever.

Q4: What precipitated the growth opportunity in the space?

I believe it’s these two trends that we’ve already discussed that contributed to the growth of outsource trading. Again, the cost pressure on asset management, and the other one is the acceleration of the work from home, or work from anywhere really, if we can call it that! I think that took an industry, this industry in particular, which has certainly existed for a number of years, but accelerated that probably forward 10 or 15 or 20 years because portfolio managers and analysts couldn’t fathom not being right down the hall or right across the desk from the trading counterparts, but then everybody learned to live without anybody when everybody was working from home. So I think those two big trends are going to continue.

Q5: Tell us about your global exposure and experience.

Most of my almost 35 years have been spent, I would say, on the international markets. And by that, I mean I’ve been focusing on markets that are located outside the United States. At Bear Stearns, as I mentioned, I started in sales on the LATAM desk, then Head of Research for LATAM, and then the Head of International Equities. And, with my partners at Bear Stearns, we had a fairly extensive expansion program going on within the equity business. I spent a number of years building out our businesses with my partners in Europe and my partners in Asia. So I traveled extensively to all those markets, probably more than my wife and my kids wanted me to be gone, but I was traveling upwards of 120-130 days a year all across the globe.

Also, with my experience at HSBC, the entire business plan at HSBC was built around the global nature of the business. Our expertise was bringing what we knew about the Asian markets, what we knew about Europe, and what we knew about emerging markets into the U.S. investment community, those that were investing outside the United States. We weren’t trying to compete with the Morgan Stanley’s, the Goldman Sachs’, or the JP Morgan’s with their U.S. equity product. We were trying to compete with what we knew from all the other international markets around the world and bringing that into the U.S. investment base.

Q6: What was the most interesting or powerful insight you learned in your career?

I’d have to say that the success in any service business is ultimately determined by your clients. It’s their trust in you and it’s their trust in your firm that ultimately determines what type of relationship you have with them. Trust is something that takes a very long time to build. But then again, you can lose it in an instant. I think you have to be very focused on doing things daily, day-in and day-out, trade by trade, making sure that you’re very focused on what this does to the long term relationship that you have with your clients.

Q7: How do you view the opportunity in the outsourced trading space over the next 3-5 years?

I’m pretty bullish on the outsourced trading space and probably the most bullish in the firm because I do believe that some of these trends that we’ve already discussed, the cost pressures and the work from anywhere culture, are things that continue to drive the business. Also, the rationalization of resources that the asset management industry is going to have to make. I think that outsourced trading makes a lot of sense and can be a natural solution for some of these challenges.

Q8: Can you speak to some of the similarities in the competitive environment of outsourced trading firms and that of what you saw over your career in traditional brokerage firms?

Certainly, client service and relationships are our key drivers to the success in both of these businesses. And specifically for trading, it’s the use of technology and how technology continues to evolve within the capital market space. But most important, I think it’s combining these two with the experiences of the traders and what the traders individually can help you do to navigate, which is already an increasingly complex environment.

Q9: What are your potential clients most concerned about, and what and how is Meraki addressing that for them?

The cost pressures are definitely the primary consideration. They may be looking at expanding into different regions of the world, and you may be able to have two or three traders for the U.S., but when you’re looking at running a 24 hour trading desk… that can get quite expensive when you talk about compliance when you talk about technology, and when you talk about personnel. I think that’s one of the reasons that they start to begin to look at outsourcing. And they’ve done that with all their other businesses- they’ve done it with compliance, they’ve done it with accounting, and things like that. I think this is just a natural extension of this.

One of the other concerns that I know that most of the people taking a look at whether or not to do this- is confidentiality. How they believe they can receive it, this outsourced trading service and still have everything that they’re doing proprietary to them and their trades proprietary to them. So I think the Meraki model fits in perfectly with that. We are more your partner. We are your licensed trader. We are not connected. We are not your custodian. We are not your prime broker. We are there solely to perform a pure buy-side trading service. And at the end of the day, you as the client, still face-off with all your counterparties across the street, and we are just there to provide you with that service.

Look, we’re not for everyone. Everybody’s not going to want to do outsourced trading, and everybody’s not going to want to do outsourced trading exactly the way that we do it. But Ben Arnold, the founder of the firm, decided this is the way we’re going to do it, and I think it’s the purest form of outsourced trading. And this is what we do. It’s the only thing we do. And it’s the only way we do it.

Q10: Why do you think Meraki ranks so high on the TRADE’s inaugural Outsourced Trading survey, garnering a 9.54 score and outperforming on the two most critical components of an outsourced trading service provider – Coverage and Execution (earning standout scores of 9.75 and 9.81, respectively)?

That’s directly related to the quality and the experience of the traders that we have on the desk. Most have over 20 years experience in some very large firms. They all have a tremendous amount of experience; they’ve seen a lot of things develop in the capital markets, they have the expertise on technology, they’re very talented deciding which way those orders should be treated because it’s not plain vanilla, it’s very complicated, and that’s the skill set that they bring to the table.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com

We are thrilled to be featured on PrimeAlpha’s Alternatives Visionaries & Innovators Podcast Series

Benjamin Arnold is the Founder and Managing Partner of Meraki Global Advisors, a buy-side solution that provides global multi-asset trading, leverage management, and capital introduction services to sophisticated and diversified clients. With an independent and unconflicted approach, Meraki helps partners manage complex strategies and asset classes across the globe.

“In my career journey, I took a unique path that led me through various roles in the finance industry. After starting at UBS Private Wealth Management, I realized I was more interested in institutional trading. Following my interest, I moved to London and interned at a firm teaching finance courses to investment bank employees. I learned about complex financial instruments and decided to pursue trading. I joined a Tiger spinout and then moved to Asian Century Quest, trading Asian equities from New York. I eventually realized I needed to be in Asia and moved to Hong Kong with my wife’s support.

After exploring different options, I ventured into sell-side trading and received multiple job offers. I chose India, where I worked at BNP Paribas and later Goldman Sachs, covering large institutions and trading various asset classes. Eventually, we returned to the US, and I founded Meraki Global Advisors, an outsourced trading firm. We started small and thoughtfully grew the business globally with offices in Park City and Hong Kong.

Our approach is different. We tailor our trading services to each client’s unique needs, fitting into their workflow instead of imposing a standardized model. We focus on bespoke solutions, supporting various asset classes and regions, and working closely with clients to provide expert trading insights. Our goal is ensuring clients have the support they need around the clock.

Looking ahead, we plan to expand our services further, including obtaining licenses for London and exploring opportunities in credit markets, crypto, and capital introduction. We’re dedicated to serving our clients’ needs and maintaining our commitment to providing trading solutions.”

Park City, New York, and Hong Kong, September 30, 2023 – Meraki Global Advisors (Meraki), a leading global multi-asset outsourced trading firm, is delighted to announce the appointment of Grace Gutekanst as the Director of Business Operations and Client Partnerships in our Park City office. Ms. Gutekanst will be instrumental in optimizing the customer experience, streamlining onboarding processes, and driving greater value in our partnerships with clients.

Grace brings a wealth of experience as a seasoned Technology and Financial professional, having successfully built out client onboarding teams with record-breaking ROI and managed over 30 technology companies and 140 private wealth management families. Her expertise and leadership in these areas have made a significant impact on the organizations she has served.

“We are thrilled to welcome Grace Gutekanst to the Meraki team,” said Benjamin Arnold, Founder and Managing Partner at Meraki Global Advisors. “Her extensive experience in technology, finance, and client relationship management will be invaluable as we continue to grow and enhance our services. Grace’s unique blend of expertise, coupled with her artistic accomplishments, reflects our commitment to diverse perspectives and holistic approaches in serving our clients.”

Prior to joining Meraki Global Advisors, Grace played a vital role as a key member of the Client Onboarding team at BBR Partners, a distinguished boutique wealth management firm located in Manhattan, NY. Throughout her four years at BBR Grace spearheaded the implementation of the client onboarding infrastructure, while also managing the firm’s clients throughout the onboarding process.

Most recently, Ms. Gutekanst held a Lead Client Success position at Nace Partners, a renowned technical recruiting firm specializing in filling high-level roles for global fintech companies. As Lead Client Success, Grace excelled in nurturing relationships with over 40 software companies on behalf of the firm’s CEO, contributing to their growth and success.

Meraki Global Advisors is confident that with Grace Gutekanst on board, the company is poised for continued growth and success in delivering innovative solutions and unparalleled client service.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com

Welcome to this episode of “Meet the Meraki Team.”

Meraki Global Advisors, a leading global multi-asset outsourced trading firm, was founded with a rebellious determination to deliver truly conflict-free services to asset managers. At Meraki Global Advisors, our team is our greatest asset, and today, we have a special guest to share his wealth of experience and expertise.

Joining us is David Laub, a seasoned trading professional with an impressive background in the investment industry. David has led trading desks and overseen various trading functions, gaining invaluable insights from both large platform funds and smaller organizations.

In this episode, David will take us through his journey, sharing valuable lessons learned and how each experience shaped his approach to trading and risk management. This promises to be a captivating conversation with a true industry expert.

“Every PM has their own mosaic about how they think of things. The best PMs are unbiased about whether they believe a stock is a long or a short; the mosaic tells them which it is. So, if we can help add a few pieces to that mosaic, then maybe we are doing our job.”

Let’s dive right in!

Q1: Walk through your history on the buyside and what roles have you filled over your career leading you to the path of outsourced trading?

I started at Hunter Global Investors, a Tiger Cub spin-out, overseeing the trading desk and other trading functions. I went to work for the individual that oversaw the financial space for an original Tiger Cub. After Hunter Global I joined a large platform fund and was there for just under 4 years.

A great benefit to being at a platform fund is that it really teaches you to be able to look at things on a relative basis. You had to be sharp because your portfolio managers were very diligent. Most platforms only allow for portfolio managers to traffic in one sector, so they become incredibly adept with all the names. For instance, some PM’s only traded tech, and others that only traded consumer, industrials, etc. but all had very tight net and gross limits that they were allowed to position around. That substantially limited them to what actions they could take, so you had to really be on top of your game as far as understanding the differences between every name in their space. So, in a way, that was my boot camp for understanding the relative world.

I was lucky enough to be approached by a gentleman leaving a macro focused firm 3+ years into the platform experience who wanted to start his own fund and offered me the opportunity to head trading there. I was with that fund for about three years. Unfortunately, the fund ran into some performance issues. It was a very good lesson in observing how portfolio managers manage risk from two different points of view, how to navigate the market itself but also how to navigate explaining their actions to investors.

All my experiences culminated in my education for how I try and help portfolio managers make sure that they’re seeing as much as possible while trying to navigate those 2 different risk points on their individual compasses.

Q2: What excited you about joining Meraki Global Advisors and outsourced trading?

It was a two-stage approach. First, I did not want to be tied to just any one manager’s performance. It can be something that is largely out of any trader’s control. You can be working with an excellent portfolio manager, who happens to be a wonderful person on top of being incredibly diligent, but there are simply unforeseen risks out there that nobody will see coming. I wanted to work to alleviate that risk. Outsourced trading was one of the best ways to do that. So, then it became a matter of doing my homework on outsourced trading.

I have good friends that are in the business. I was privy to a fair amount of information about how it worked, where people had strengths and weaknesses. When I came across Meraki, I liked the strength this firm has demonstrated internationally. The two founding members have spent significant time internationally, which I thought is a competitive advantage.

Q3: With that diverse skill set, tell us what areas of the market or the hedge fund trading landscape you focus on now.

It depends on the portfolio manager that you’re working for. Where we find one can add the most value is this: if the portfolio manager is not keen to focus on risk metrics, we will try to add that to their perspective by monitoring and highlighting those we think may be impacting the portfolio. For instance, if you get a good fundamental bottom-up stock picker, and the PM knows the five or six names they really like but are exposed in just two sectors, are they aware of their concentration risk? If they are limited on sector risk by their mandate, then they will be, but if not, will their investors allow for this? We are keeping an eye on those things so that they don’t get to the point where their exposure is too concentrated, especially for sophisticated investors.

Now if we are trading for someone that is coming from a well-known platform, then they are already focused on that. We find that people from platforms are much more focused on what others are thinking about their space. Most of the platform spin outs are exposed to multiple risk factors that control their optionality in whatever sector they are trading. They get it on managing their risk.

A large majority of the PMs are talented enough to have succeeded to such a level that they are now able to open their own shop. They know their names as well as any on a fundamental basis, so many look for an edge. That edge seems to reside somewhere between trading flow and game theory. The structure of the platforms comes into play here. If there are 4 or 5 large platforms that all have at least 3 or 4 portfolio managers in each sector, the total number of pods trading the same space can easily reach 15 or 20. If each pod has an AUM roughly around $500M, then that quickly adds up to multiple billions watching and trading a sector with itchy trigger fingers.

These PM’s would like to know what will make the others in the space take action. What is enough to force others to trade and then be able to take that same action just before whatever catalyst that is the game theory thesis. This concept makes them much more sensitive to what the chatter is around each and every name, what other investors are saying around those names and the flows in each name that follow. So, of the 20 people trading one name, it’s ok to be the 3rd, 4th, or 5th to take the same action, but being 18th or 19th would be costly if the name is overtly consensus.

So, the answer to the focus depends on whether it is more of a fundamentally focused portfolio manager or a platform-oriented one that’s already been exposed to the circus.

Q4: How do you differentiate yourself with your buy-side background relative to others?

This can be a nuanced question from the standpoint that there are lots of very good people out there. I worked with plenty of very talented people at a platform, but I got the subjective feeling that so many were focusing on the minute relative differences of their sectors. Since they are surrounded by magnificent risk departments, they have no reason to take a step back and try to see things through a more holistic lens.

One of the ways that I try to differentiate is to make sure that I can add value to a portfolio manager that might need it, in places where they might have blind spots. Every PM is different; they all have their own methodology and the way they approach things. I have been fortunate enough to have traded for a lot of different styles of portfolio management. If I can identify a stylistic tendency that often generates a blind spot, I can then try and fill that blind spot. Some will accept it, some may value it, and others could think it’s worthless. But I have found that going through the pattern recognition exercise, whether they find value or not, still gives me the opportunity to mention something that may help with their mosaic. They may not see the value that I do, but one has to try.

Q5: As an outsourced trader, how do you view risk, both at the stock level and the portfolio level?

We try and help portfolio managers focus on the metrics we are familiar with. It’s not for us to opine on risks related to the fundamentals, that is the domain of portfolio managers and analysts. What we can try and bring to light is overextended names in the portfolio and or names we think demonstrate crowdedness.

When portfolio transparency is available from the client, we can rank the portfolio through a few different metrics. None of these metrics in and of themselves can offer the answer as to whether a name is overextended, but together they can help offer a view as if they may be.

We start by ranking the relative strength index of each name. It is not always the case but names with RSI’s over 70 or below 30 are often thought to be over extended. We also like to look at what the option market is telling us. If the implied volatility is substantially higher than the historic volatility, are we aware of why? Is there a forthcoming binary catalyst? If so, is the portfolio manager comfortable with the potential negative outcome? So, we rank the difference between the implied and historic volatilities of each name in order to try and spot any outliers. Finally, we monitor the alpha and beta contributions to overall performance. If a particular name has an unusually large contribution of alpha, could that mean that the market is overly confident in the name presently, and if expectations are not met is it susceptible to a reversion?

All 3 of these metrics can help us alert portfolio managers if each of them is leaning a certain way. A name with unusually high RSI, low implied vol and extreme alpha contribution headed into a quarterly earnings report should have a very good result. But, if the name were to miss it would be at risk, much more so than a name without the 3 metrics ranked as highly. On the flip side, and this is where we have found this exercise to be even more valuable, is when the set up is around consensus short names. If the RSI ranks very low, the performance contribution is highly driven by beta or nonexistent alpha, and implied vol is very low, it could become a recipe for an upside surprise. If in fact the name is a consensus short, it becomes a very dangerous candidate for a short squeeze.

Portfolio risk is something we can look at, but that is largely the domain of each individual portfolio manager. Given full transparency we will always monitor sector, geographical and factor risk, but it has been our experience that most PM’s are fully aware of these metrics from day one of their launch. As we mentioned from the beginning, we are simply trying to offer a view to our clients that they normally might not have in their focus.

Q6: When you speak with a fund with a trading-focused portfolio manager, how might you engage?

A lot of younger portfolio managers and those with large platform experience are very informed in trading. They may have much shorter holding periods in mind, which makes any pertinent information related to their names even more impactful in the short term. A few ways we can try to help add value are: (1) keeping them abreast of all order flows that could impact their names either directly or indirectly. (2) offer anything that’s tertiary, anything that feels like it offers them an edge. (3) Once in a while, remind them that fundamentals can matter, especially when many are so focused on every little screen movement. For the most part, the trading-oriented PMs know what they want to do; all you can do is try and add as much color as possible.

Q7: On the flip side, if a fund is looking for less noise on the trading front but more core competencies from you, how do you tailor the information you push through to them?

Tread lightly. One does not need to be an all-star when trading things for them, especially if a PM sends an order with instructions to trade it as you see fit. You need to slowly figure out what their time sensitivity is and how their vocabulary works. Traders and portfolio managers sometimes have different vocabularies, and it’s very important to start and be extra careful when you are first learning the tendencies of new portfolio managers. From there, we try and introduce different things to see what resonates at a slow pace. This is where the metric rankings and a few other things that we do for portfolio managers come into play. If any of it resonates, we will continue to do it. If it does not, we simply block and tackle the best we can.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com

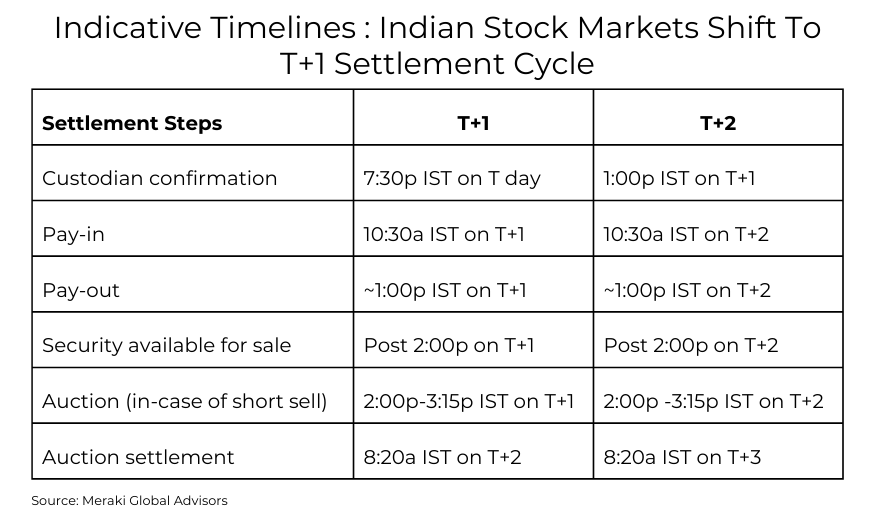

On January 27, 2023, India’s exchanges completed the phased monthly transition from a T+2 to a T+1 settlement cycle for all top-listed securities, which includes shares, exchange-traded funds (ETFs), real estate investment trusts (REITs), infrastructure investment trusts (InvITs), sovereign gold bond (SGB), government bonds, and corporate bonds trading in the equity segment. While most large stock markets, like in the US, Europe, and Japan, still follow a T+2 settlement cycle, India will join China in shortening its settlement cycle. Chinese stocks on the exchange markets settle T+0 for securities and T+1 for cash.

The settlement cycle transition is expected to benefit investors by working to increase market liquidity while reducing settlement risk. A shortened cycle not only reduces settlement time but also reduces and frees up the capital required to collateralize that risk. While this has halved the settlement time for equities in India, it has presented its own set of challenges for Asset Managers (AMs) without a presence in the Asian region. Meraki will examine how this new rule, with just over a half year in existence, has affected AMs in their trading workloads and increased time spent by their staff.

Complications for Asset Managers Operating in Distant Time Zones

The impact of the shift to T+1 will not be uniform across all firms. Smaller firms, in particular, may face greater difficulties due to the disparities in the size and locations of their teams. With reduced settlement times, these firms may experience an increase in settlement fails, as their teams may struggle to keep up with the faster pace of trade settlement during irregular business hours. Furthermore, smaller firms often rely on legacy batch overnight systems that may not be equipped to handle the increased volumes that will come with T+1. Therefore implementing new systems capable of managing the higher transaction volumes will be necessary, leading to additional operational infrastructure (headcount and IT) costs for these firms.

At the crux of the change is the trade confirmation timeline and FX/funding needs. The change in pay-in/pay-out timings simply means that timelines are now reduced by one day. Previously, stocks were settled by approximately 2pm IST on T+2; now, they settle at 2pm on T+1, and all other settlement related timelines will move forward similarly. Please see the indicative timelines below:

Confirmation of trades by custodians must be done on T-day before 7:30p IST (previously 1:00p on T+1), and the confirmation of trades takes place only after the trade is matched and the FX/funds are in place. With a T-day timeline, clients must now give the FX and matching instructions either pre-trade or during the day. This is typically done by generating a trade and currency file to the custodian after the close in order to generate proper FX amounts and allow for trade matching on the execution side. Because the INR is restricted, only the custodians can trade FX on behalf of the client.

Execution and Settlement Complications

On the execution side, traders may need to stop trading before the close or prefund their onshore accounts. Prefunding onshore accounts in INR opens the asset managers to FX risk that they otherwise would not have taken in order to deliver INR on time for funding their trades. Additionally, the AMs need to invest further in headcount or find current employees willing to work live Indian hours to solve settlement and funding issues on a T+0 basis in order to abide by new exchange rules.

Outside of the explicit operational costs, there is a considerable risk of burnout, trading and operations team fatigue, and other issues that arise from live trading and operational needs for a market that has the last and latest opening time of every major APAC regional market and also closes a full 12 hours after Australia opens for trading in the region. The typical workarounds utilized include handing India off by the Asia teams to the European teams when they arrive in the morning, or if there is not a dedicated live trader or trading team and operations team for each region, the Asia time zoned teams stop trading the India markets early. Some traders working both shifts even take a nap for a few hours and wake up to finalize the T+0 matching process. All these scenarios can lead to operational problems, poor trading execution, missed liquidity, and possible errors that can potentially prove costly. In addition, trader burnout and high rates of employee turnover may be common with this trading arrangement.

How Meraki Can Help

Given India’s nuanced nature, our expertise in all aspects of trading, settlement, and funding in India is unmatched, and we have the local resources and knowledge to expeditiously solve problems as they may arise. Meraki’s Founder and Managing Partner, Benjamin Arnold, traded for BNP Paribas and Goldman Sachs on the ground in India for four years and then another two years from Hong Kong. Meraki’s Head of APAC Trading, now based in Hong Kong, lived and traded in India for two years for a global investment bank.

Additionally, our unique outsourced trading agreements with our clients allow us to execute on behalf of the investment manager and/or fund(s). In contrast, our primary competitors cannot do so as effectively, placing us in a differentiated and superior position during communications with sell side trading desks, custodians, banks, and investment managers. Meraki Global Advisors’ seamless business structure allows the investment manager to save explicit costs on personnel and IT, as well as mitigating concerns of burnout and quality of life that arise from India’s unique and new trading requirements and distant time zone.

Please contact Mary McAvay at mm@mga-us.com to discuss how Meraki can work closely with you to help solve your Indian trading issues.

The investment industry refers to outsourced trading as a trading relationship in which the investment manager gives its portfolio order to broker-dealer counterparties to execute on their behalf. What gets lost in this casual understanding is the inherent conflicts of interest that may exist when giving their counterparty these orders with respect to best execution, payment for order flow, and information leakage. The industry has warped the true meaning of outsourced trading into a homogenous term making it easy to confuse broking with outsourced trading, as both involve the handling of orders for further trading/execution and anonymity for moving orders.

Key differences exist between a fully integrated buyside outsourced trading desk and a traditional wrapped brokerage service offered by multi-service providers. In a fully integrated outsourced trading desk relationship, the trader serves as a partner, engaging in trading communication, understanding and communicating information to investment managers to further the investment thesis, and ensuring multiple venues and algorithmic infrastructure are in place to facilitate best execution. Unlike services from large broker-dealers, there is no payment for order flow, no internal crossing of order flow, no principal order book, and no incentive outside of getting the best execution for the buyside client. In addition, the end client can be linked to the commission wallet, which can help access the deal calendar and brokerage research resources. Trust is a critical component of this partnership, as the portfolio managers must have confidence in the provider’s ability to act on its behalf, handle trades in specific ways, and align its interests with those of the fund.

Understanding Brokering: Traditional Broker Services

In its traditional sense, broking refers to the intermediation services brokers provide in facilitating trades between buyers and sellers. Brokers act as intermediaries, executing orders on behalf of clients and earning commissions or fees in return. These services typically include trade execution, market research, access to liquidity, and limited ancillary functions. They can also refer to payment for order flow, which is an ancillary financial benefit a broker can earn from their customer’s order flow.

Unveiling Outsourced Trading: Redefining the Approach and Investment Manager Considerations

Outsourced trading represents a paradigm shift from traditional broking arrangements. It involves delegating trading operations to specialized firms that offer a comprehensive suite of services beyond execution. Outsourced trading providers provide expertise, technology, and operational efficiency, acting as strategic partners rather than traditional brokers.

Outsourced trading enables the investment manager to earn credit for commissions from executing brokers and to properly allocate its commission wallet across the street, which can help on the deal calendar.

It allows for transparency during block trading and bid-wanted situations so the broker can price large trades with tighter spreads.

Outsourced trading allows the trader to act as a true extension of the investment process and to become fully integrated into risk and trading conversations at the individual stock level as well as at the portfolio level.

For a client seeking access to a specialized broker they don’t currently work with, it’s not as simple as picking up the phone and placing a trade. There are onboarding procedures that need to be followed, including KYC (know your customer), AML (anti-money laundering), connectivity, and contractual matters. However, due to the nature of their business, an outsourced trading provider is better equipped to gain access to that specialist broker.

The Benefits of Outsourced Trading Over Broker Services

Outsourced trading offers numerous advantages that set it apart from traditional broker services:

Enhanced Efficiency

Outsourced trading firms provide a holistic solution encompassing trade execution, risk management, compliance, and technology integration. This streamlined approach optimizes operational efficiency and allows asset managers (“AMs”) to focus on core competencies.

Cost-effectiveness

By outsourcing trading operations, investment managers can minimize the need for substantial investments in trading infrastructure, technology, and talent acquisition. Outsourced trading providers offer scalable solutions, enabling asset managers to expand their trading capabilities without incurring significant fixed costs.

Access to Expertise and Technology

Outsourced trading firms bring specialized knowledge, market insights, and advanced technology platforms to the table. This empowers asset managers’ investment management team(s) with real-time data, advanced analytics, and cutting-edge tools, facilitating informed decision-making.

Risk Management and Compliance

Outsourced trading providers specialize in navigating complex regulatory frameworks and employ robust risk management systems. They work to ensure compliance with regulatory requirements, transaction reporting, and best execution practices reducing institutional risk exposure.

Types of Outsourced Trading Firms

Outsourced trading firms can be categorized based on their areas of specialization:

Full-Service Providers

These firms offer end-to-end trading solutions, encompassing trade execution, risk management, compliance, technology integration, and post-trade support.

We at Meraki Global Advisors, a prominent outsourced trading firm, are known for our comprehensive global range of services. With a deep understanding of global markets, Meraki provides tailored solutions for equities, fixed income, foreign exchange, derivatives, and all other asset classes. Our expertise extends beyond execution, encompassing risk management, compliance, technology integration, and strategic guidance, making us an ideal partner for investment management teams seeking efficient and scalable trading solutions.

Specialized Providers

These firms focus on specific asset classes, trading strategies, or geographic regions. They offer targeted expertise and tailored solutions to cater to the unique needs of asset managers operating in those domains.

Expands the Fund’s Expertise and Widens its Reach

Outsourced trading represents a departure from traditional broking arrangements, offering asset managers a range of benefits beyond execution. A diverse outsourced firm can provide geographical expertise, asset-type expertise, or both to existing trading desks looking for specialization or funds looking for a fully outsourced model.

A diverse outsourced firm should feel as comfortable trading US equities as it does trading CDS or Asian OTC derivatives while understanding the market limitations and requirements to execute these instruments in each location. In turn, delivering knowledge and experience to the fund manager allows them to capitalize on certain investment opportunities or understand liquidity constraints, reducing valuable time spent researching ideas that are not applicable to their liquidity constraints.

As the demand for outsourced trading increases, Meraki continues to expand and meet the needs of our clients to help them achieve their goals. In just four years, we have expanded globally from our US headquarters and team with best-in-class global multi-asset buyside traders and middle-back-office support. We have also proudly maintained an industry-low client-to-trader ratio critical to providing a truly integrated relationship and premium service. We recognize that outsourcing may be a significant change for some funds; we are eager to speak with any managers interested in learning more about the advantages of outsourced trading and the suite of services provided by Meraki Global Advisors.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com

Scott Kurtis Joins Meraki Global Advisors as Chief Operating Officer

Park City, New York and Hong Kong, May 9, 2023 – Meraki Global Advisors (Meraki), a leading global multi-asset outsourced trading firm, today announced that hedge fund veteran Scott Kurtis has joined the firm as Chief Operating Officer.

In Scott Kurtis’ new position, he will oversee Meraki’s financial, operational, and administrative functions; this includes governance and execution of systems and processes that support its growing outsourced trading mandates. Among his responsibilities, he will be implementing processes and technology that leverage data to drive efficient operations.

“In his position as COO, Scott Kurtis will focus on innovation, process improvement and efficiency across our global offices. His extensive background trading globally across many asset classes for both traditional and hedge fund investment managers, and his wide-ranging experience in operational and technology functions will play a major role in propelling our firm into the future,” said Benjamin Arnold, Founder & Managing Partner of Meraki.

To date, Kurtis’ hedge fund industry career has focused on trading, technology, treasury functions, middle and back-office operations. He’s well-versed in internal and external audits, compliance, operational assessments, process improvement, software selections, outsourced C-Suite management, risk management. Specific risk expertise centers on portfolio, operational and counterparty risk.

Most recently, Kurtis worked as a Senior International Trader for Artisan Partners and Harris Associates where he specialized in European and Asian equities. Previous positions also include serving as Director of Operations, Head Trader, and Partner at Asian Century Quest Capital (ACQ), a New York-based hedge fund focused on Asian investments with satellite offices in Hong Kong and Tokyo. During ACQ’s nine-year growth from $5 million to $2 billion in assets under management, he built the fund’s operational framework, risk management systems, and treasury operations. Prior to ACQ, he worked as an Asian trader for Maverick Capital and as an international sales-trader for Goldman Sachs in Chicago.

He earned his MBA from the Kellogg School of Management in 2018 and graduated from Northwestern University in 2001 with a BS in Journalism and a dual degree in Economics. He received the 2000 Vandy Christie Award for outstanding loyalty and dedication to the tennis program as a member of the varsity tennis team.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com

Tom O’Leary Joins Meraki Global Advisors as a Senior Business Strategist

Park City, New York and Hong Kong, February 2023 – Meraki Global Advisors LLC (Meraki), a leading global multi-asset outsourced trading firm, today announced that Tom O’Leary has joined the company as a Senior Business Strategist. O’Leary will be responsible for advancing Meraki’s strategic growth plans by emphasizing and aligning the key functions of strategy planning, business development, and process improvement.

“The need for a sophisticated outsourced trading service capable of trading all asset classes globally is only increasing as asset managers contend with competitive pressures, growing cost burdens, and sub-optimal trading operations,” said Benjamin Arnold, Founder and Managing Partner of Meraki Global Advisors. “Tom is a seasoned Wall Street executive with a strong strategy orientation who has deep industry experience and a proven track record leading major initiatives and businesses at premier global investment banking and capital markets firms. The growth of the company internally reflects Meraki Global Advisors’ client expansion globally, supporting the increasing demand for our differentiated and premium outsourced trading services.”

O’Leary brings over 35 years of extensive industry experience in strategic planning and business development, leading high performing teams, and integrating information technology for improving processes at companies building and scaling their capital markets business infrastructure. He joins Meraki from HSBC Global Banking and Markets, where he served as Managing Director and Head of Equities for the Americas focusing on managing the equities business across the globe, and a member of the Global Equity Executive Committee. Prior to HSBC, O’Leary was a Senior Managing Director with Bear Stearns in a variety of leadership positions, including Co-Head of the Global Equity Sales Division and Head of International Equities.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com

The Benefits of Having a Local Presence in the Asia-Pacific Region

For asset management firms based outside the APAC region, trading APAC markets is a challenging mosaic of regulatory, operational, and tactical matters. In such an environment, entrusting asian orders to brokers overnight and expecting the best execution outcomes has been proven to be inconsistent at best.

Building and staffing an in-house off-hours trading desk or an entire regional office has historically been the solution, but the associated costs are often prohibitively high. As a result, many firms have chosen to engage with an outsourced trading provider to optimize performance.

Due to the fragmented and competitive nature of trading in Asia, firms must take extra care to ensure goodness-of-fit with an outsourced trading provider. It would be beneficial to ask the following questions while assessing your outsourced trading provider: Is the provider truly positioned to succeed in the challenging Asian markets? Will the provider be a trustworthy partner and experienced guide in complicated conditions?

In our experience, successful trading in Asia demands three core capabilities: (1) Careful management of order flow; (2) Deep, localized knowledge and (3) Well-established relationships. Here we explore several characteristics of Asian markets and illustrate how these core capabilities build a foundation for success.

Less liquidity for block trades

Sourcing liquidity presents different challenges in Asia than in the US and Europe. In Asia, most names are less liquid, and many countries lack dark pools – making block trades particularly challenging.

On-the-ground experience is essential when navigating difficult liquidity landscapes. Firms engaging with outsourced trading providers should ensure their assigned traders are well versed in the idiosyncrasies of each country where securities are being actively traded, including facilitation risk options and regulations. Equally important, are close relationships with sell-side connections and local brokers for both color and liquidity. Traders with deep relationships will benefit from timely updates on blocks as well as impactful news and flows – an advantage that carries significant value.

Additionally, traders must pay special consideration to information sharing, judiciously choosing how much information is shared and with whom. While certain block desks are consistent performers, there is always risk of leakage, which can be very impactful in most Asian markets.

More volatility driven by governance and event risk

Careful management and trading of order flow is important in all markets – but even more so in Asia, where governance and event risk can be significantly more common and corrosive, driving intraday price swings that often dwarf those seen in the US and Europe. As such, the trust required to handle order flow in the most appropriate manner is higher in Asia than developed markets. If a trader simply inputs orders into an algorithm with little care or attention, the results in Asia are likely to be sub-optimal.

Diverse market structures and regulations

Given that Asia lacks a single regulatory framework – in the way MiFIDII provides structure in Europe, for example – traders are faced with a diverse array of market structure dynamics. Without the operational expertise, ever-changing regulations can prove to be complicated.

When confronting this challenge, local knowledge and relationships are of the utmost importance. To ensure timely notification of regulatory changes and potential impacts, firms should identify a trading partner who is entrenched in the local markets and connected with the street and various levels of people within relevant organizations. A broker who may be insufficiently familiar with market structures and regulations can create a range of problems, including issues with entry and exit of positions and trade settlement.

Greater retail participation

Retail participation is generally much higher in Asia than developed markets. The Chinese equity market, for example, is largely dominated by retail investors: More than 70% of turnover originates from retail participants, relative to approximately 15% to 20% in the US.

In markets with size-able retail participation, news reported in the local language can impact markets before it reaches primary information streams, such as Bloomberg and Reuters. This is particularly true in China, Hong Kong, Japan, and South Korea. Additionally, local blogs and news sharing apps can generate huge retail interest, as does the morning hard-copy news in China.

This dynamic creates additional opportunities and risks for offshore institutional investors. Given the profound impact retail trading can have on short-term price momentum in Asian markets – for both single names and indexes – traders must be able to provide real-time explanations and interpretations of themes which have captured the attention of a given retail audience. Such capabilities stem from deep, localized knowledge and a broad network of relationships.

Improve your APAC trading with Meraki Global Advisors

The Meraki team has the expertise and access required to trade every asset class worldwide, including all markets in Asia. Our senior leaders draw on extensive experience in the region:

Donald Lee, Head of Asia Pacific and Head of Meraki Global Advisors (HK) Ltd – Don has over 27 years of experience in Asia Pacific institutional equities split between Seoul and Hong Kong. Before joining Meraki, Don held senior management positions in the APAC -wide cash equities and client executions businesses of Credit Suisse and Deutsche Bank based out of Hong Kong.

Jeffrey Ho, Managing Director of Meraki Global Advisors (HK) Ltd – Jeffrey has over 25 years of buy-side experience trading global markets in Europe and Asia. Before joining Meraki, Jeffrey was a trader at Tora Outsourced Trading, Segantii Capital Management, and prior spent 15 years at Deutsche Bank (DB) in Hong Kong where he was a Director and Senior Trader.

Benjamin Arnold, Founder and Managing Partner – Ben previously worked as Executive Director on the equity and equity derivatives sales-trading desk at Goldman Sachs in Hong Kong and Mumbai, India with a primary focus on large non-ECM block trading. Before joining Goldman Sachs, Ben was a Vice President on the equity and equity derivatives sales-trading desk at BNP Paribas in Mumbai.

EJ Stockley, Partner and Global Head of Trading – EJ previously worked as a trader at First State Investments in the UK and Singapore, gaining global multi-asset trading experience in Pan-Asian, EMEA, and Americas markets.

Simon Kelt, Head of APAC Trading – Simon has over 15 years’ experience trading global markets in both Europe and Asia. He spent the last 10 years in Asia across Hong Kong and India, most recently at HSBC trading Asian equities with a focus on greater China market coverage where he helped develop and build out the business.

How Meraki Global Advisors can help

As a value-added service to our outsourced trading clients, we help managers create a strategic marketing strategy and increase their firm’s awareness among a unique set of investors and allocators. Our experienced team provides start-up advisory services, identifies actionable ways to improve decks and pitches, and creates prospective allocator lists for select introductions. Our services are suited for a diverse range of clients, extending from traditional long-short emerging managers in the very early stages to managers running a multi-strategy platform and existing multi-billion-dollar funds trading globally across asset classes.

As the premier global multi-asset outsourced trading firm, we take pride in putting our clients’ interests first. Built on a foundation of confidentiality, our unique conflict-free model empowers funds to garner optimal access to liquidity.

Contact us to learn more about Meraki Global Advisors’ outsourced trading capabilities and capital introduction services.

About Meraki Global Advisors

Meraki Global Advisors was founded with a rebellious determination to deliver truly conflict-free services to asset managers. Headquartered in Park City, Utah with offices in New York and Hong Kong, Meraki provides outsourced global multi-asset trading, leverage management, and capital introduction services to the asset management industry. Meraki Global Advisors LLC is a FINRA member and SEC Registered. Meraki Global Advisors (HK) Ltd is licensed and regulated by the Securities & Futures Commission of Hong Kong.

For more information, visit the Meraki Global Advisors website and LinkedIn page Contact: Mary McAvey VP of Business Development (646) 666-7041 mm@mga-us.com